Clemenger Media Sales, CMS, Clemenger Consulting, Clemenger is advertising, marketing, media buying, media buying agency: if you want to buy media, advertising, if you want to buy radio advertising, buy magazine advertising, do you want to buy digital media, are you buying TV advertising, or want content marketing, media sponsorship – Clemenger can help you. We give you the above / this news to help you learn / live / continually improve (call or email if you need help with your media / advertising / marketing investment (we are Australia’s home to niche media :

The 80/20 View: Australia is about to enter a boom ad market – here’s why

In his regular column for Mumbrella, media analyst Ben Shepherd looks ahead to analyse the advertising market against a volatile climate.

Predictions are a dangerous game. If you’re found to be right no one remembers, and if you’re wrong your misjudgement is documented for all to see.

This column is all about finding the insight in the signals and data that exist around us. And from looking closely at a bunch of health, vaccination, economic, consumer confidence and retail spending data, my view is we are about to head into a very strong 12 months for the advertising market.

This acceleration is likely to happen from November onwards, and if we can find a way to successfully navigate the health and logistics challenges that more movement creates, there’s a high chance based on the data available that this acceleration can sustain through to Christmas in 2022.

Until November, my view is the market will be flat.

It’s not going to go backwards, but the comparison to the same period in 2020 will likely be low single digit increases. This prediction is driven by a few key data points.

For one, consumer confidence is subdued at present. Look at the dip from April. A reduction in consumer confidence means people start to close their wallets, defer larger investments in bigger household purchases (more on this later). Given the drop in confidence coincided with Delta ravaging NSW and Victoria, it’s hard to think this confidence will bounce back until we have some quantified milestones that demonstrate we’ve wrestled back control of the virus. Again, this is likely to be in November.

Source: Trading Economics, September 2021. [Click to enlarge]

Source: Trading Economics, September 2021. [Click to enlarge]

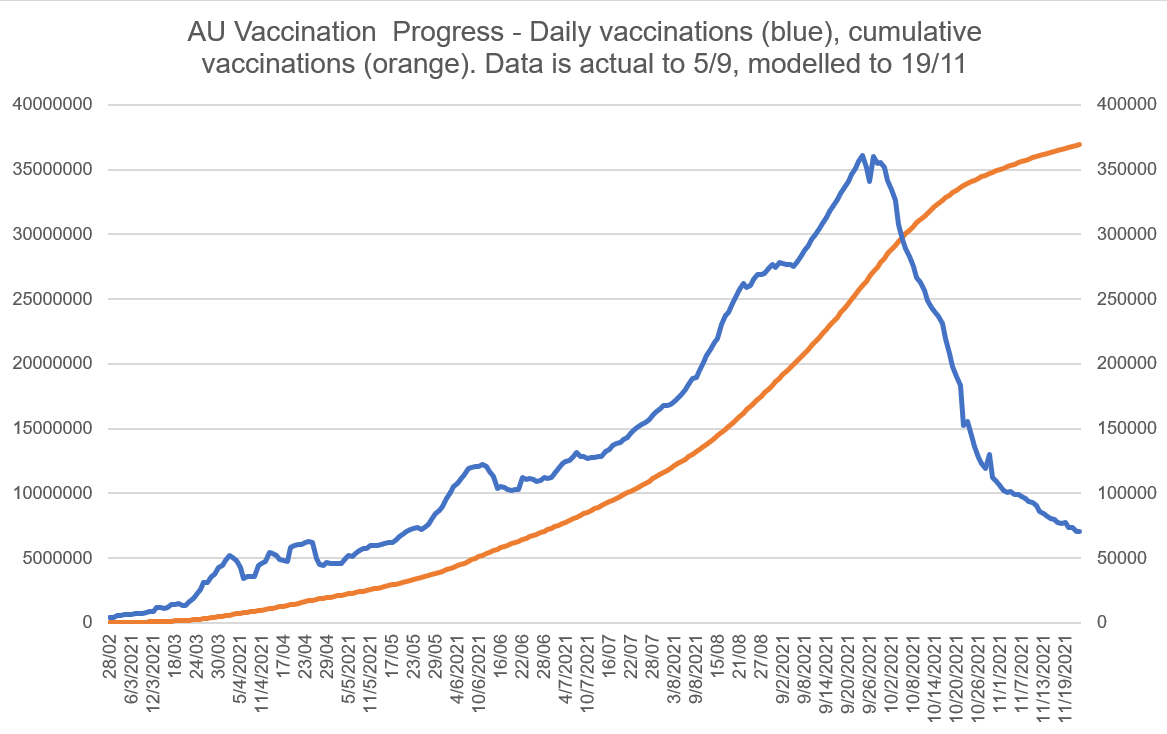

The consensus is Australia will be at around 80% double jabbed by mid November.

Most models doing the rounds at the moment suggest 80% will have two jabs by mid November. I ran a model on the weekend based on the Canadian rollout and modelling the Australian rollout post-5 September, based on how Canada behaved. The reason for this is, to date, Canada and Australia have had a very similar rollout. Steady and methodical. The difference is Canada started a few months before us.

Source: Australian Government 2021, Canadian Government 2021, Data is actual to 5 September, modelled by author from 6 September – 23 November.

Basically, my model demonstrated that daily vaccinations will peak in late September and we will hit 80% of 12+ on Melbourne Cup Day. Add two weeks for vaccines to become effective, and we are likely to safely hit the 80% threshold by 16 November.

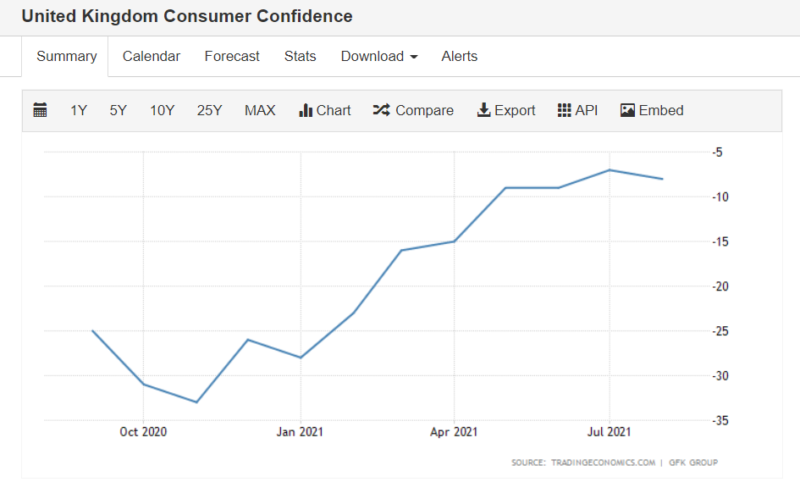

If we follow the lead of the UK, consumer confidence will bounce once we hit a vaccination threshold or around 60% of the total population.

The UK saw similar declines in consumer confidence to Australia with the onset of COVID, however confidence dipped again with the Autumn wave of cases and fatalities. However, once the UK generated real momentum with its vaccination efforts (February/March), consumer confidence began to rapidly increase, as the below table shows.

Source: Trading Economics, September 2021. [Click to enlarge]

The current economic hesitation from consumers is around the immediate term, driven by increased cases and the wait for vaccination. Once these two metrics improve, consumer confidence is likely to spike quickly.

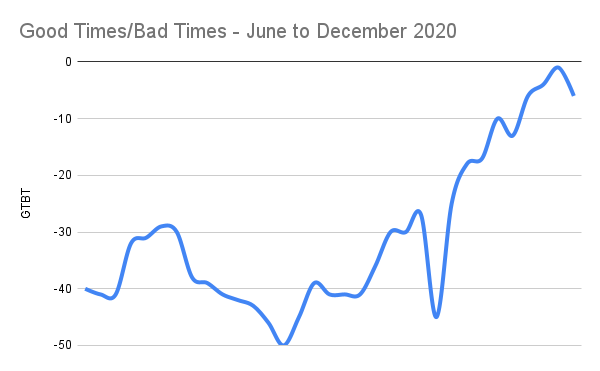

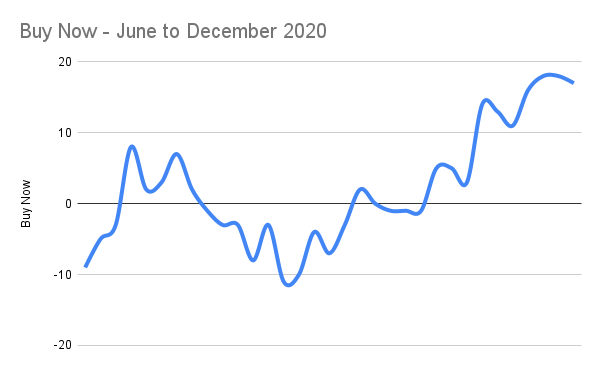

Australia’s drops in confidence in 2021 have been related to two very specific areas – the perception around good or bad times over the next 12 months, and the sentiment around whether right now is a good time to buy major household items.

The good news is year on year, these metrics are up.

Source: Roy Morgan ANZ Consumer Confidence Index, September 2021.

Source: Roy Morgan ANZ Consumer Confidence Index, September 2021.

The bad news is they’ve been dropping consistently over the past 8-12 weeks and have moved from general optimism to general pessimism. Any value under zero means there’s more bears than bulls.

The good news is we saw in 2020 that when borders opened and lockdowns ceased, these two measures in particular rebounded very strongly. Below is the Good Times/Bad Times and Buy Now index tracked from June-December 2020.

Source: Roy Morgan ANZ Consumer Confidence Index, September 2021.

Source: Roy Morgan ANZ Consumer Confidence Index, September 2021.

We see in the last quarter of the year a big bounce. My view is this will occur again from November.

Why? Because people have money in the bank. Even though they’ve dropped since pandemic highs, savings levels remain high across the board.

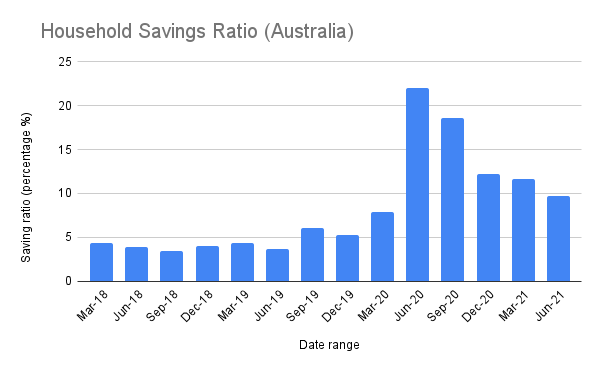

Check the below table, it outlines savings as a ratio of income in Australia.

Source: Australian Bureau of Statistics August 2021.

This ratio peaked in the June and September quarters of 2020, but has remained just above or just below 10% since. For perspective, pre-COVID the household saving ratio was consistently below 4%.

This means there’s a lot more money in savings accounts than there was before COVID. By November we will have had around 22 months where household savings have been 2-4x their normal levels. History would suggest once consumers feel optimistic, they will look for ways to spend this money.

We even saw in late C20 that once optimism and confidence returns, consumers are happy to dip into these savings. This boosted retail growth to levels no one predicted.

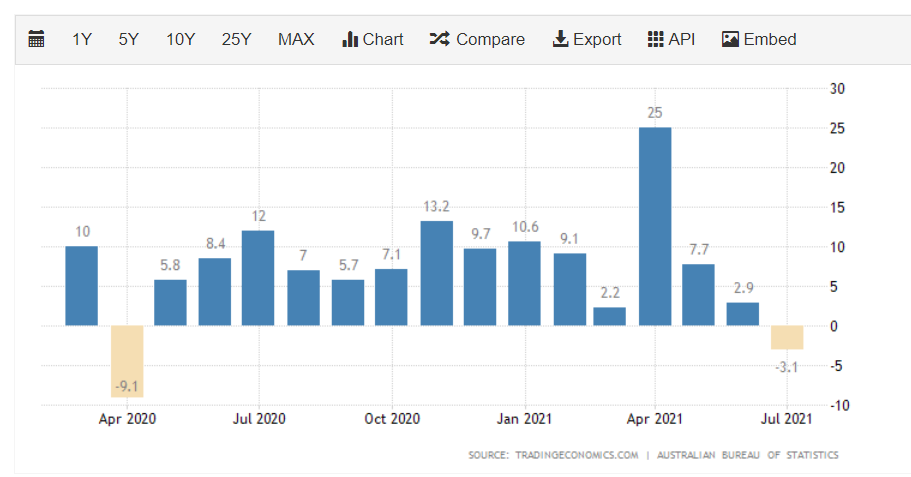

The below outlines year on year retail sales growth from March 2020 to July 2020.

The only blip was April 2020, which saw a decline in retail spend. The other months saw year on year increases compared to the same period in 2019. July 2021 saw retail spend go backwards, but the comp is important. This is being compared to a booming July 2020 which was up 12% on the same month in 2019.

The most important numbers to look at below are the October-December retail growth numbers, these increased by 7-13%

Source: Trading Economics, September 2021. [Click to enlarge]

E-commerce will remain a massive focus – the expectation is that the recent growth will continue. However, this growth will need fuel.

E-commerce growth will be a prime focus for all retailers – given a slowing in growth, it’s likely these retailers will need to invest more in marketing to drive demand. The largest beneficiaries are likely to be the platforms.

The below outlines non-food e-commerce retail consumer spending since the beginning of 2016. The blue line represents spend by month, the red line represents year on year increase as a percentage.

Source: Australian Bureau of Statistics September 2021. [Click to enlarge]

On top of all this, two big advertising sectors are primed for a big 12 months – travel and automotive.

Travel advertising has basically stopped since March of 2020. Airlines, hotels, comparison sites, travel insurance, tours, cruises … a huge sector that has basically stopped on a dime.

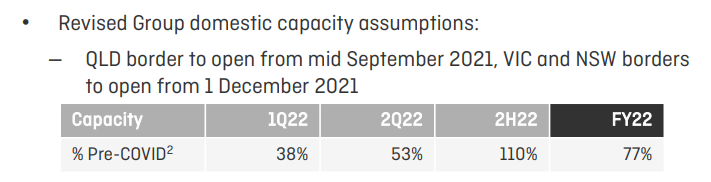

If you take Qantas’s guidance in their recent earnings report, they are preparing for a big increase in passenger load. The guidance suggests that December will be almost at normal capacity in terms of domestic volume, and the second half of FY22 will be 10% above normal capacity on domestic routes.

Source: Qantas Group Results Presentation August 2021.

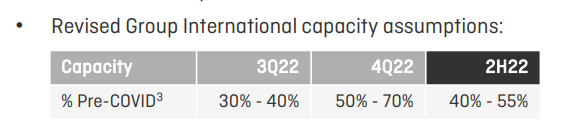

Qantas is also bullish about international capacity. It’s likely to ease back in Q3 of FY22, across the March quarter, and then increase almost double again in the June quarter.

Source: Qantas Group Results Presentation August 2021.

Now, this is only one data point. But it is the nation’s biggest airline and one of the most high profile travel brands in the world saying it feels very confident that the tourism business will start to bounce from December onwards. This has a flow on effects for hotels, tour operators, entertainment, leisure, cafes and hospitality. All industries that have been in a holding pattern.

It’s realistic to believe that from November, tourism advertising will begin to increase to create demand for this opening up.

Automotive is also likely to want a slice of increased consumer savings too.

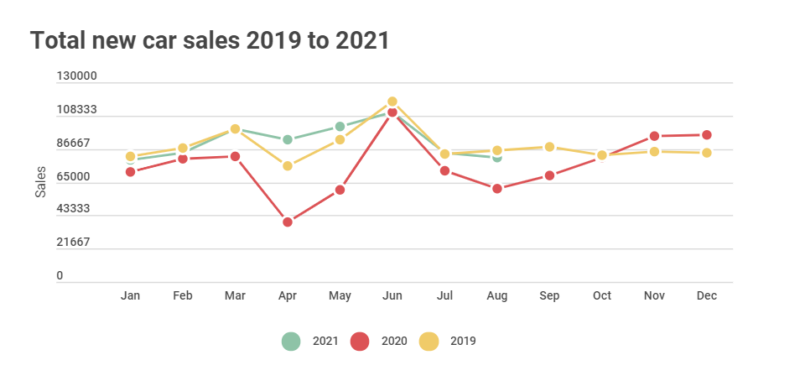

Below shows car sales 2019-2021. Across the back quarter of 2020 and into the first half of 2021, automotive sales had bounced nicely from the lows of 2020. However, from June this growth has dipped and August sat under what was a pretty lethargic same month in 2019.

Source: VFACTS, taken from CarAdvice September 2021

Consumer confidence undoubtedly is impacting automotive sales. The hope for most OEMs will be that a boost in confidence, combined with a boost in savings volume, will boost the market from November onwards and into 2021. This will likely require increased advertising from November onwards. On top of this, in the December quarter of 2020, OEM’s dramatically increased their advertising investment, with TV and paid search being the main beneficiary. All indicators point to this happening again.

All of these elements point to an advertising boom from November 2021 onwards, right through 2022.

My view is there’s a lot of signals which suggest above average growth in the advertising market is ahead of us. Higher confidence, higher vaccination rates will drive confidence. Confidence will unlock the base of household savings. And categories like travel, entertainment and tourism, which have been dormant for so long, will come back to life.

For media companies, this will mean crafting and sharpening their proposition to take advantage of this future growth. The companies that will achieve above market growth will be able to link their ability to impact consumers with their ability to quantify their contribution to sales and revenue.

My view is the big winners over the next 14 months will likely be the ones who will be the winners over the next 5 years. The prize is out there – who’s going to grab it?

Ben Shepherd is a media analyst. The 80/20 View is a regular column on Mumbrella.